Donating real estate to charity

A tax-smart approach to maximize your philanthropic impact

by the Charitable Strategies Group at DAFgiving360®

Whether it’s the family home, undeveloped land, a rental property, or some other investment, your real estate held for more than one year may be the most highly appreciated asset you own. This means you could face significant capital gains taxes if you sell your real estate.

Depending on your particular financial and charitable goals, donating real estate to a 501(c)(3) public charity, such as a donor-advised fund, could allow you to leverage one of your most valuable investments to achieve maximum impact with your charitable giving.

Benefits of contributing real estate to a DAF

Donating your real estate can unlock additional funds for charity in two ways. First, you potentially eliminate the capital gains tax you would incur if you sold the real estate yourself and donated the proceeds, which may increase the amount available for charity by up to 20%. Second, you may claim a fair market value charitable deduction for the tax year in which the gift is made and may choose to pass on that savings in the form of more giving.

Donor-advised fund sponsors, which are public charities, provide an excellent gifting option for contributions of real estate, as the funds typically have the resources and expertise for evaluating, receiving, processing, and liquidating this type of gift.

Disclosure: Please be aware that gifts of appreciated non-cash assets can involve complicated tax analysis and advanced planning. This article is only intended to be a general overview of some donation considerations and is not intended to provide tax or legal guidance. In addition, all gifts to donor-advised funds are irrevocable. Please consult with your tax or legal advisor.

Case study: selling property vs. donating property

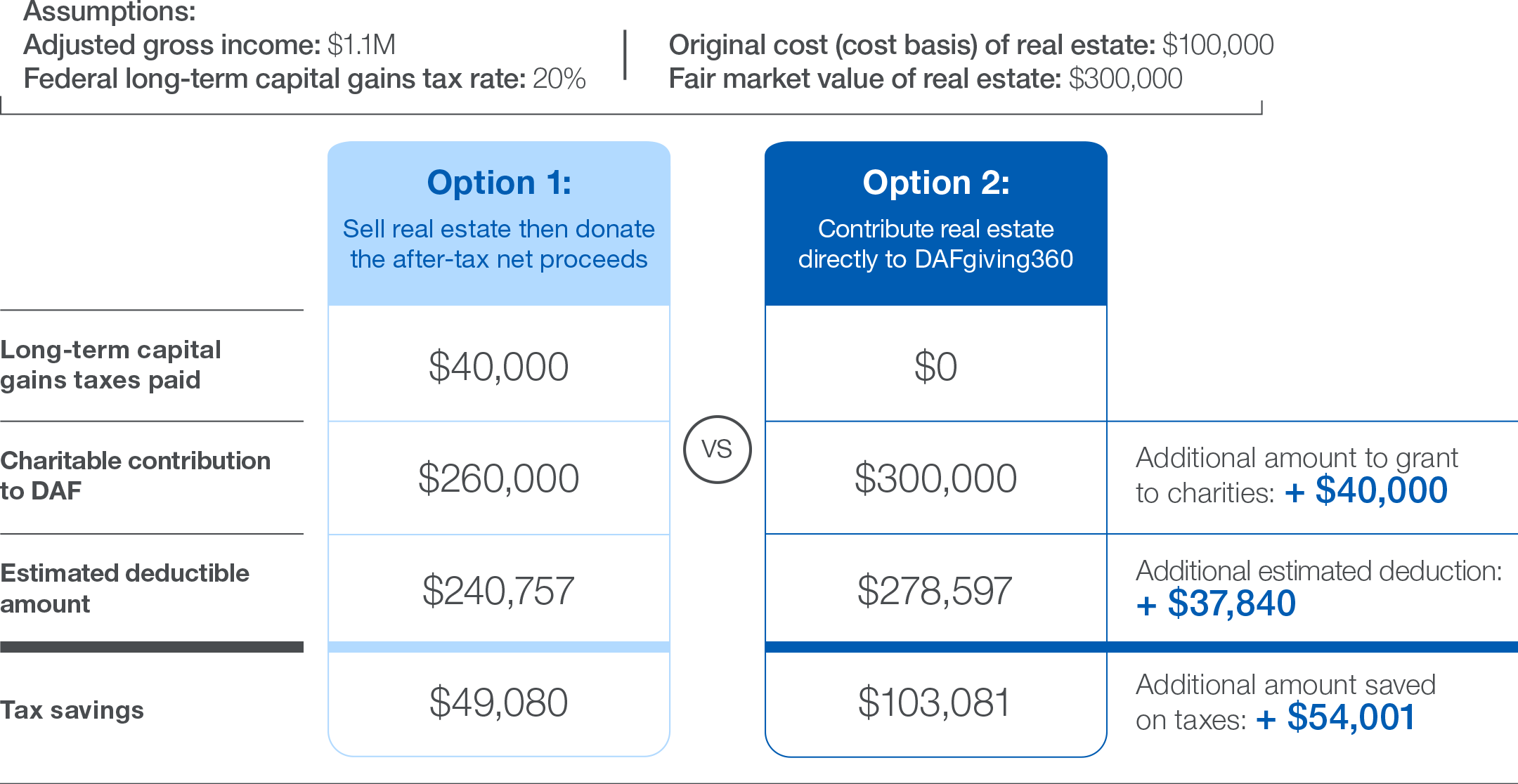

To illustrate the benefits of donating appreciated property, consider Jim, who is approaching retirement and considering donating his single-family rental property he inherited from his parents 25 years ago.

Jim’s adjusted cost basis of the rental is $100,000.

The property has appreciated $200,000 for a current estimated value of $300,000.

Jim’s adjusted gross income (AGI) is $1,100,000. Assume a 20% federal capital gains tax rate based on Jim’s income level.

Tax note: For taxpayers who itemize, only the portion of total charitable deductions for the year that exceeds 0.5% of AGI is deductible. In Jim’s case, this reduces his allowable deduction by $5,500 ($1,100,000 x 0.5%). See IRC § 170(b)(1)(I).

Tax note: For taxpayers in the top tax bracket (above 37%), IRC Section 68 effectively caps the value of itemized deductions at 35%. In Jim’s case, this further reduces his tax-deductible amount as illustrated below.

Option 1: Jim sells the rental property first and then donates the net cash proceeds to charity. If Jim sold the rental property, he would owe an estimated $40,000 in federal long-term capital gains taxes ($200,000 x 20% = $40,000). After paying the federal capital gains taxes, Jim’s estimated net cash available for charitable giving is $260,000. After Jim donates the cash, Jim is eligible for a $240,757 tax deduction. This reflects his $260,000 contribution, reduced by $5,500 (0.5% of AGI floor), and the $13,743 IRC §68 limitation.

Option 2: Jim could instead donate his rental property to a donor-advised fund or other public charity to potentially eliminate federal capital gains taxes of $40,000. This increases Jim’s charitable contribution to the full $300,000 value of the rental property (based on a qualified appraisal). After Jim donates the rental property, Jim is eligible for a $278,597 tax deduction, reflecting the $300,000 contribution reduced by $5,500 (0.5% of AGI floor) and the $15,903 IRC §68 limitation. * In this option, Jim has an additional $40,000 to grant to charities and an additional $37,840 estimated deductible amount.

This example is for illustrative purposes only. It does not take into account state or local taxes or Medicare and net Investment Income tax. The estimate assumes a single charitable gift, no other itemized deductions, no carryforward and incorporates deduction limitations such as the 0.5% AGI floor (IRC § 170(b)(1)(I)), applicable AGI limits for gifts to charities, and the IRC § 68 reduction. The tax savings shown is the estimated deductible amount, multiplied by 37%, minus the long-term capital gains taxes paid. Gifts of real estate require a qualified appraisal to determine fair market value. Actual deduction availability and tax benefits depend on individual circumstances and applicable limitations. Consult a tax advisor regarding your individual situations

Important considerations when donating real estate

In addition to the potential tax benefits described above, the following considerations may apply.

1. Donate marketable real estate.

You may consider contributing real estate to charity as long as the charity can sell the property in a timely manner (i.e., it is a marketable property and relatively easy to liquidate). In addition, it makes sense to donate real estate where:

The property has been held for more than one year and has appreciated significantly.

The property is debt free. If there is debt on the property, you may be subject to IRS “bargain sale” rules, which can generate some capital gains tax and lower the value of your charitable deduction. In addition, the debt may be taxable to the charity when the property is sold (e.g., acquisition indebtedness).

You are willing to transfer the property irrevocably to the donor-advised fund or other public charity, which will negotiate the sale price and control the sale, often using an experienced intermediary.

2. Avoid prearranged sales.

If a sale is expected prior to your charitable contribution of real estate, then the terms of the sale should still be under negotiation. The documentation must not have proceeded to the point at which the IRS would consider it a prearranged sale. In that unfortunate instance, the IRS may deem your donation an “anticipatory assignment of income” to the charity. As such, you may be required to pay capital gains taxes when the real estate is sold by the charity.

3. Qualified appraisal requirements and annual deduction limits apply.

Overall deductions for donations to donor-advised funds are generally limited to 50% of your adjusted gross income (AGI). The limit increases to 60% of AGI for cash gifts, while the limit on donating appreciated non-cash assets held more than one year is 30% of AGI. The IRS permits a carryover for five tax years, should your charitable deduction exceed AGI limits in a given tax year.

To substantiate your charitable income tax deduction, you are required to complete Form 8283 and obtain a qualified appraisal from a qualified appraiser for contributions of real estate in excess of $5,000.

Interested in learning more?

The Charitable Strategies Group at DAFgiving360 is a team of professionals with specialized knowledge about non-cash asset contributions to charities. Our team stands ready to support you and your advisors, from initial consultation through asset evaluation, receipt, processing, and sale. We strive to provide unbiased guidance and frequent communication at every step of the process to help you and your advisors make informed decisions and stay aware of the time required for your transaction.

For more information about the advantages of contributing appreciated non-cash assets, you can read an overview article or call us at 800-746-6216.

If you would like to learn more about donor-advised fund (DAF) accounts with DAFgiving360, click here.