Donating IPO stock to charity

A tax-smart approach to maximize your philanthropic impact

by the Charitable Strategies Group at DAFgiving360®

If you hold equity in a fast-growing private company, such as an artificial intelligence (AI) or technology company, you may be approaching a potential liquidity event like an initial public offering (IPO).

An IPO can accelerate appreciation of private company stock held by founders, executives, and early employees. High appreciation before or after the IPO may result in a wealth event with substantial capital gains taxes when you sell shares of the stock. Donating shares before or after an IPO may provide a unique opportunity to leverage one of your most valuable investments to maximize your gifts to charity while reducing your tax burden.

Types of IPO stock you may be able to donate

Pre-IPO stock generally refers to shares of a private company before it becomes publicly traded. Founders, executives, early employees and investors may hold significant appreciated value in privately held business interests, including shares acquired through equity compensation awards.

Post-IPO stock generally refers to shares of a company that has completed its IPO and is publicly traded on an exchange. Following an IPO, charitable giving may create opportunities for tax-efficient planning and portfolio diversification — especially by helping offset gains when unwinding concentrated stock positions.

Donor-advised funds can often accept both pre-IPO and post-IPO stock, although the timing, valuation, transfer process, and tax considerations may differ depending on the type of asset and the company’s circumstances. See the considerations below for more information on donating shares of pre-IPO and post-IPO stock to charity.

Benefits of contributing IPO stock to a DAF

Donating IPO stock can unlock additional funds for charity in two ways. First, you potentially eliminate the capital gains tax you would incur if you sold the shares yourself and donated the proceeds, which may increase the amount available for charity by up to 20%. Second, if the shares have been held for at least one year, you may claim a fair market value charitable deduction for the tax year in which the gift is made and may choose to pass on that savings in the form of more giving.

Donor-advised fund sponsors, which are 501(c)(3) public charities, provide an excellent gifting option for donations of IPO stock, as they typically have the resources and expertise for evaluating, receiving, processing, and liquidating this type of gift.

Disclosure: Please be aware that gifts of appreciated non-cash assets can involve complicated tax analysis and advanced planning. This article is only intended to be a general overview of some donation considerations and is not intended to provide tax or legal guidance. In addition, all gifts to donor-advised funds are irrevocable. Please consult with your tax or legal advisor.

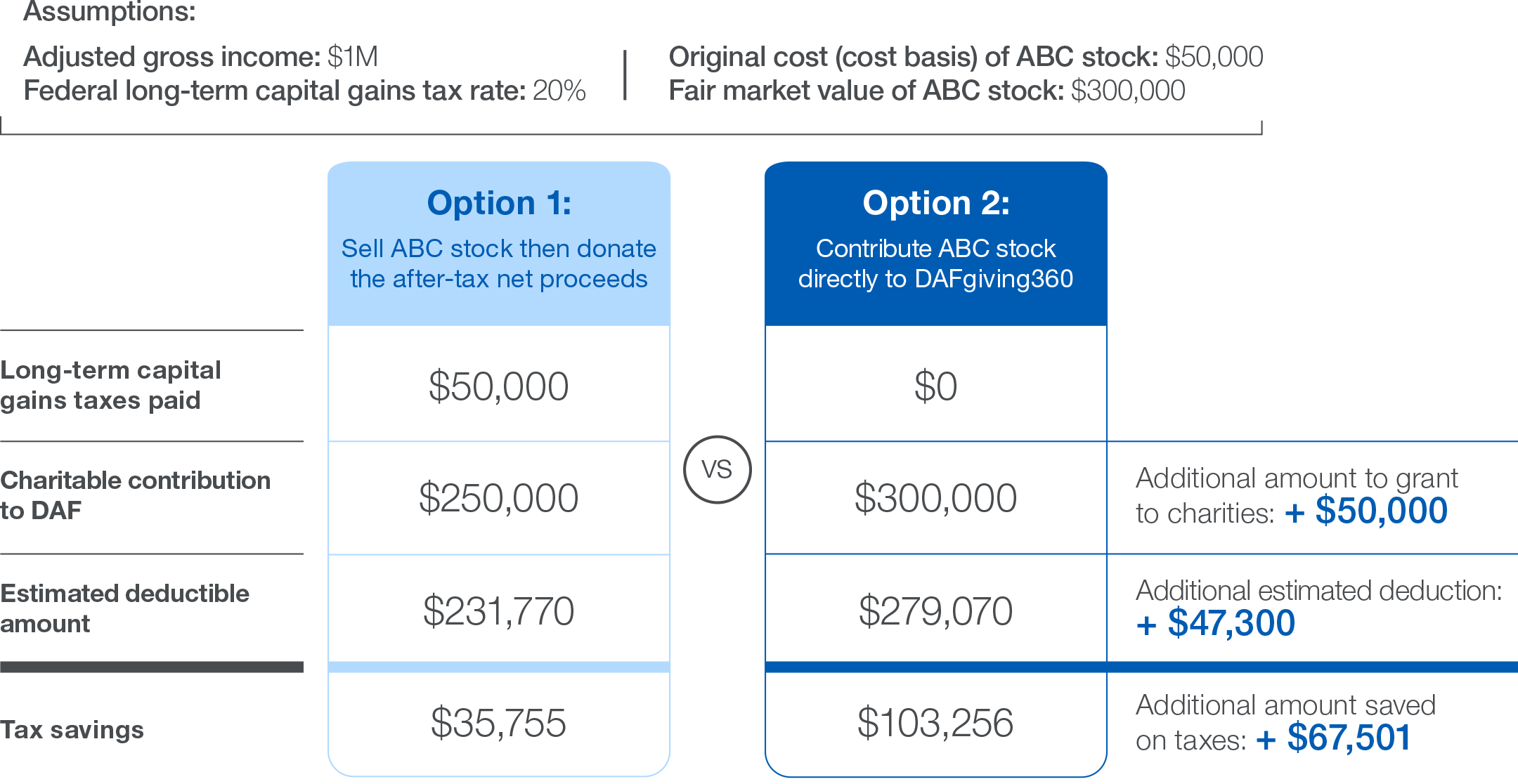

Case study: selling IPO stock vs. donating IPO stock

To illustrate the potential benefits of donating appreciated IPO stock, consider Sarah, an early employee of ABC, a startup tech company, who received incentive stock options a few years ago. Following the company’s IPO and significant post-IPO appreciation, and with the six-month lock-up now expired, Sarah plans to contribute a portion of her shares to a donor-advised fund (DAF) and recommend grants to her favorite charities over time.

- Sarah exercised stock options several years ago and purchased shares for $50,000 at $16.67 per share.

- After the IPO, the stock rose to $100 per share for a total fair market value of $300,000, a gain of $250,000.

- Sarah’s adjusted gross income (AGI) is $1,000,000, and her federal capital gains tax rate is 20%.

- Tax note: For taxpayers who itemize, only the portion of total charitable deductions for the year that exceeds 0.5% of AGI is deductible. In Sarah’s case, this reduces her allowable deduction by $5,000 ($1,000,000 × 0.5%). See IRC § 170(b)(1)(I).

- Tax note: For taxpayers in the top tax bracket (above 37%), IRC Section 68 effectively caps the value of itemized deductions at 35%. In Sarah’s case, this further reduces her tax-deductible amount as illustrated below.

Option 1: Sarah sells her stock first and then donates the net cash proceeds to charity. If Sarah sold the stock, she would owe an estimated $50,000 in federal long-term capital gains taxes ($250,000 x 20% = $50,000). After paying the federal capital gains taxes, Sarah’s estimated net cash available for charitable giving is $250,000. After Sarah donates the cash, Sarah is eligible for a $231,770 tax deduction. This reflects her $250,000 contribution, reduced by $5,000 (0.5% of AGI floor) and the $13,230 IRC §68 limitation.

Option 2: Sarah donates her stock directly to a donor-advised fund or other public charity. In this scenario, Sarah avoids paying the $50,000 capital gains tax. This allows Sarah to contribute the full $300,000 fair market value of ABC stock. After Sarah donates the stock, Sarah is eligible for a $279,070 tax deduction, reflecting the $300,000 contribution reduced by $5,000 (0.5% of AGI floor) and the $15,930 IRC §68 limitation. ¹ As a result, Sarah has $50,000 more available to grant to charities and approximately $47,300 of additional deductible value compared to selling the stock and donating cash.

Disclosure: This example is for illustrative purposes only. It does not take into account state or local taxes or Medicare and net Investment Income tax. The example assumes a single charitable gift, no other itemized deductions, single filer status, no carryforward and incorporates deduction limitations such as the 0.5% AGI floor (IRC § 170(b)(1)(I)), applicable AGI limits for gifts to charities, and the IRC § 68 reduction. The tax savings shown is the estimated deductible amount, multiplied by 37%, minus the long-term capital gains taxes paid. Actual deduction availability and tax benefits depend on individual circumstances and applicable limitations. Consult a tax advisor regarding your individual situation.

Important considerations when donating IPO stock

In addition to the potential tax benefits described above, the following considerations may apply.

1. Donate long-term held shares with high appreciation.

In order to realize maximum tax savings from a charitable donation of stock, the incentive stock options for the shares must have been held more than one year from exercise date and two years from grant date. In addition, the shares should have appreciated in value. Shares not meeting these criteria do not carry the same tax advantages.

2. Donating private shares before an IPO requires due diligence by the charity and careful planning by the donor.

Many charities do not accept gifts of private stock before an IPO due to the complexity involved. Donor-advised funds and other public charities that do accept these gifts likely will do so only after performing due diligence. For example, the company’s governing documents — such as shareholder agreements, operating agreements, bylaws, etc. — must be reviewed to understand whether there are any transfer restrictions or embedded liabilities, and to assess the timeline and process to complete the charitable transfer.

For gifts of private shares in excess of $5,000, the IRS requires donors to obtain a qualified appraisal by a qualified appraiser to substantiate fair market value for the charitable deduction. Appraisals must be obtained no earlier than 60 days before the date of donation or no later than the due date of the donor’s tax return (including extensions) for the year of the gift. Appraisals depend on the facts and circumstances at the time of contribution and may be discounted for lack of marketability and/or lack of control.

The above are only some examples of many possible considerations when donating private shares. Please consult your tax advisor prior to making these donations.

3. Be mindful of lock-up restrictions.

The decision of whether and how charitable gifts of IPO stock may be made during a lock-up period is determined by the issuer’s counsel. In cases where gifts of IPO stock can be made during a lock-up period, any restrictions that materially affect the value of the shares or prevent the shares from being freely traded may require a qualified appraisal to substantiate the fair market value, and such restrictions may lead to valuation discounts.

You should work closely with the donor-advised fund or other public charity when you transfer stock subject to a lock-up. Your stock donation is irrevocable and you cannot dictate the timing of the sale. DAFgiving360’s ordinary policy is to immediately liquidate stock, but exceptions to this rule may apply. Please consult with your corporate counsel and the donor-advised fund or other public charity when donating stock during an IPO.

4. Consider whether Rule 144 legend and affiliate restrictions apply.

If your stock is restricted by legend or is “control” stock owned by an affiliate of the issuer (i.e., you are an officer, director, or 10% shareholder), then your company’s general counsel must give you permission to transfer the stock to charity. As a general rule, restricted stock must be sold in accordance with Rule 144 resale restrictions. ²

Contributions of long-term held restricted stock to a public charity, including a donor-advised fund, may be deductible at fair market value as of the date of contribution, but valuation discounts may apply if restrictions are not lifted prior to gifting. A qualified appraisal may be required to substantiate the fair market value.

To learn more about gifts of restricted stock, click here.

5. Avoid prearranged sales.

You should not enter into any arrangement that would legally compel the donor-advised fund sponsor or other public charity to dispose of the stock upon receipt. This kind of “prearranged sale” could reduce or eliminate the tax benefits of making your donation. Upon receipt of the stock, the donor-advised fund or other public charity controls the asset. For most donor-advised funds and other public charities, the general policy is to promptly sell appreciated securities, but a charity may reserve the right to sell at any time.

6. Annual limits apply to charitable deductions.

Overall deductions for donations to donor-advised funds are generally limited to 50% of your adjusted gross income (AGI). The limit increases to 60% of AGI for cash gifts, while the limit for appreciated non-cash assets held more than one year is 30% of AGI. The IRS permits a carryover for five tax years, should your charitable deduction exceed AGI limits in a given tax year.

Interested in learning more?

- The Charitable Strategies Group at DAFgiving360 is a team of professionals with specialized knowledge about non-cash asset contributions to charities. Our team stands ready to support you and your advisors, from initial consultation through asset evaluation, receipt, processing, and sale. We strive to provide unbiased guidance and frequent communication at every step of the process to help you and your advisors make informed decisions and stay aware of the time required for your transaction.

- For more information about the advantages of contributing appreciated non-cash assets, you can read an overview article or call us at 800-746-6216.

- If you would like to learn more about donor-advised fund (DAF) accounts with DAFgiving360, click here.