Bunching charitable contributions

Maximizing tax benefits by concentrating or “bunching” charitable contributions

Using both the standard deduction and itemized deductions

Coauthors:

Caleb Lund, CAP®

Director of Charitable Strategies Group

DAFgiving360TM

Hayden Adams, CFP®

Director of Tax Planning and Wealth Management

Schwab Center for Financial Research

Download a PDF of this article

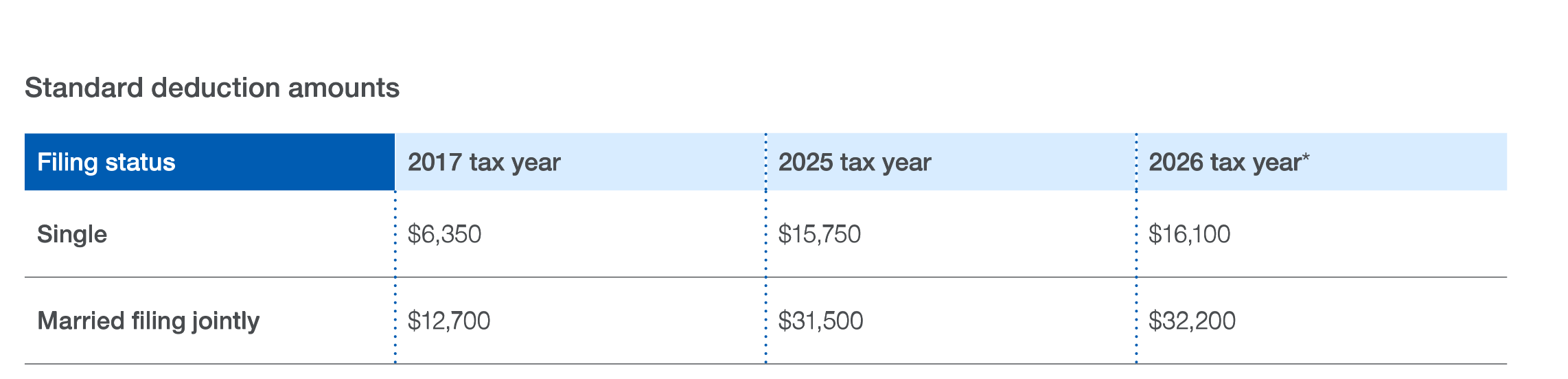

The standard deduction has more than doubled since enactment of the Tax Cuts and Jobs Act in 2017. Because of these increases, many taxpayers who historically itemized deductions may find it advantageous to take the standard deduction in the future. Those who are charitably inclined and find themselves on the margin between taking the standard deduction or itemizing could maximize their tax benefits by “bunching” two years of charitable contributions1 into one year, itemizing deductions for that year, and taking the standard deduction the next year.

-

*The inflation-adjusted standard deduction amounts for the coming tax year are announced every October or November.

1 Overall deductions for donations to donor-advised funds and other public charities are generally limited to 50% of your adjusted gross income (AGI). The limit increases to 60% of AGI for cash gifts, while the limit on donating appreciated non-cash assets held more than one year is 30% of AGI. The IRS permits a carryover for five tax years, should your charitable deduction exceed AGI limits in a given tax year.

Case study: how exactly does this bunching strategy work?

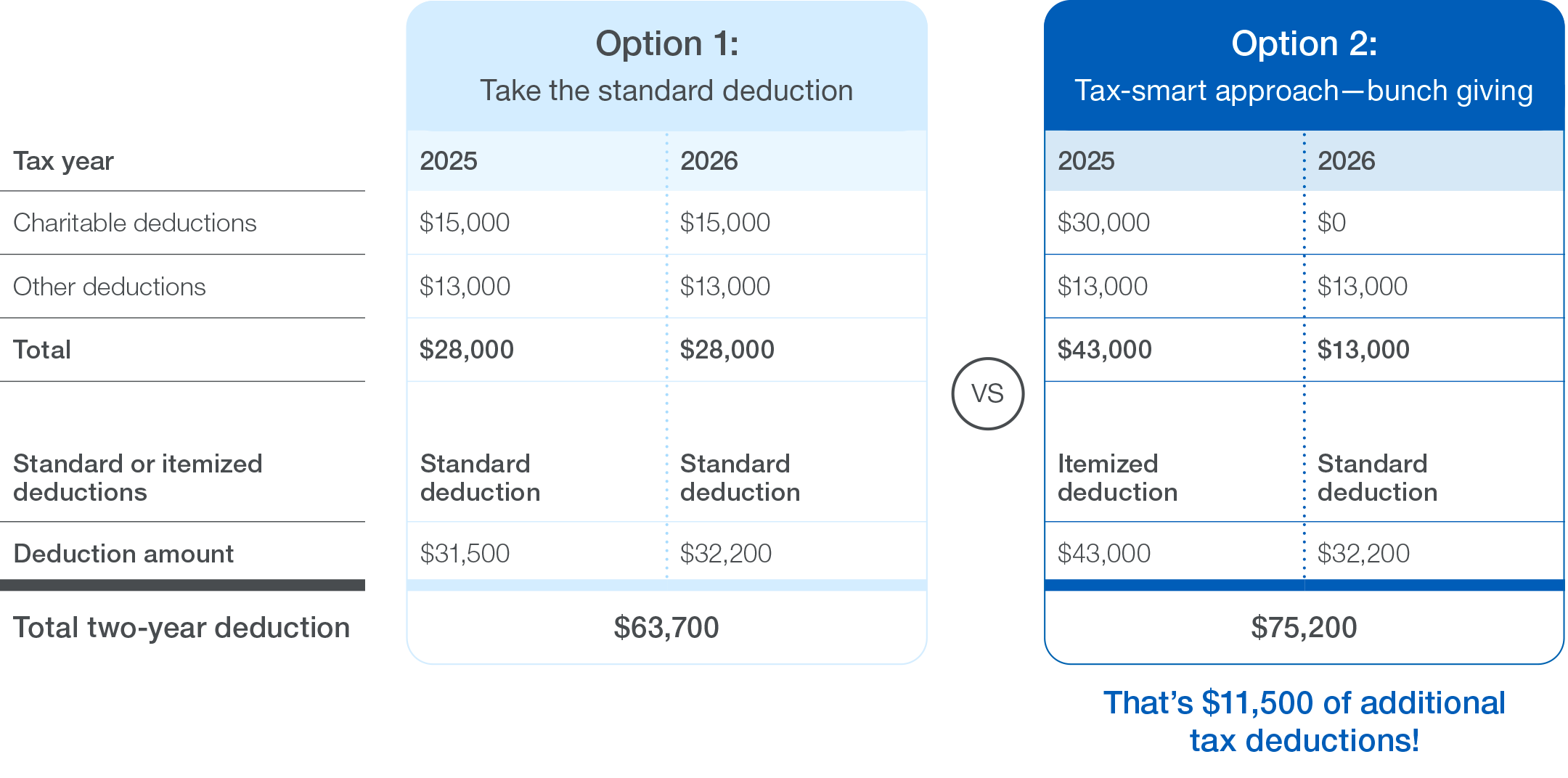

Alison and James are a married couple filing jointly with no children. Annually, they have $28,000 of itemized deductions, including $15,000 in donations to a donor-advised fund.

Option 1: Because their total deduction amount is below the standard deduction for both 2025 and 2026, Alison and James could take the standard deduction each year, and over two years they would claim a total of $63,700 in standard deductions.

Option 2: However, if Alison and James instead decide to take a more tax-smart approach and bunch their donations into a single year, they could end up with a larger overall deduction for that same two years. Rather than donating $15,000 to charity each year, the couple donates $30,000 in 2025, making their itemized deductions for that year total $43,000. Then in 2026 they take the $32,200 standard deduction. With this option, the couple has $11,500 of additional tax deductions over the two years. In addition, if these contributions were made to a donor-advised fund account, the couple could recommend grants to charity in each tax year.

-

This hypothetical example is only for illustrative purposes.