Charitable estate planning checklist

When it comes to preparing for the future, most people think about taking care of loved ones. They already know that it’s critical to have an estate plan. But what if your legacy could extend even further? With charitable estate planning, you can support the causes you care about long after you’re gone. Whether you have a will, trust or a complex estate plan, adding charitable giving strategy is simpler than you might think.

When considering a charitable giving strategy, we encourage you to speak with your financial advisor and estate planning attorney about your specific situation.

Let's talk estate planning with charitable goals. Remember to check these five things off your list. First, estate plans usually start with clear definitions. A will is the cornerstone foundation document, and without one, state law decides how assets are divided up, which may not align with your values or priorities. Second, clarify what you want your charitable impact to look like. Advisors and heirs can use this information to set up or continue your giving and fulfill your values beyond your lifetime. Third, consider how a donor-advised fund account might be used. What is a donor-advised fund, or DAF, as it's sometimes called? It's a simple, tax-smart investment solution for charitable giving. After opening a DAF account, you can make irrevocable contributions during your lifetime, or at death, and may be eligible to claim a tax deduction for them. Contributions to a donor-advised fund account may also be invested for potential growth that's tax-free, helping you to have more to grant out to charities over time. Fourth, it's also important to be strategic when deciding which assets to contribute to DAF and which go to other beneficiaries. Choosing the right assets to fund a donor-advised fund account can maximize charitable impact and minimize tax liability. And fifth, work with the donor-advised fund sponsored charity to create succession plans for your DAF. A DAF can extend your charitable values well beyond your lifetime, but only if you've created a plan for what comes next. If you want to learn more about charitable estate planning, you can get more details in the full article.

Who needs charitable estate planning?

Without an estate plan, decisions about your assets, including who inherits and manages what and how much goes to each person or organization, may be made by a probate court, which might not make decisions according to your wishes. A clear, personalized estate plan increases the odds of a smooth transfer of your assets.

The stakes are even higher for individuals or families with significant wealth. Without a thoughtful plan, tax obligations and legal complexities can needlessly erode the wealth you intend to pass on.

For those who are philanthropically minded, charitable estate planning is equally beneficial. Charitable estate planning is the process of incorporating charitable giving goals into your long-term financial and legacy strategy.

For example, a charitable estate plan might include:

Leaving a specific gift to charity (e.g., $100,000 cash)

Naming individuals to succeed you on the DAF account and continue your charitable giving legacy

Naming a DAF as beneficiary of a retirement account, and using the DAF account for a one-time gift or ongoing gifts to charity

Setting up a charitable remainder trust (CRT) or charitable lead trust (CLT), which can combine gifts to charity with income to heirs

These strategies integrate within overall legacy planning to potentially reduce estate and income taxes, streamline transfers, and create a lasting impact.

To help you develop a clear charitable estate plan, this sample checklist highlights how to blend tax-smart charitable giving strategies into your estate plan so that you can make a philanthropic impact for generations to come.

Charitable estate planning checklist

1. Establish a will and/or revocable trust and designate charitable beneficiaries

Estate plans usually start with clear definitions: a will is the cornerstone foundation estate planning document that declares who should receive what and when, and who should be named as executor (the person you trust to manage the process for settling your estate). A will is important because it’s used to name heirs, choose guardians for your minor children, and outline your final wishes. Without a will, state law decides how assets are divided up, which may not align with your values or priorities.

For additional control and privacy, consider creating a revocable living trust. Unlike a will, a trust avoids the time and expense of probate and can also be useful during life to clarify how you want your assets owned and organized. After the trust is drafted and signed, be sure to fund your trust by changing the title of assets and property you want the trust to own. Otherwise, assets not properly owned by the trust lose the benefits revocable trusts offer.

For financial accounts (e.g., brokerage, IRA), life insurance, and other pay-on-death assets, you should review the beneficiary designations. Effective use of beneficiary designations enables your estate to side-step probate, gets assets directly to your heirs or a favorite charity, and can save you on time and expenses. Note that beneficiary designations and accounts with survivorship will override any conflicting provisions in a will or revocable trust. We recommend reviewing your account titles and beneficiary designations whenever there is an update to your estate plan.

2. Clarify your charitable goals

When integrating charitable goals into your estate plan, you need to define the values and causes you want to support. Some questions to consider: What are you most passionate about? What kinds of donations feel most meaningful to you?

Don’t know your charitable goals? That’s okay. Set aside some time to sit down, be alone and consider the key events in your life or talk with loved ones to have them involved in the philanthropic legacy you want to leave. You might also consider drafting a charitable giving mission statement for your family and advisors.

Ultimately, your charitable goals should align with your personal purpose and your desired legacy. This plan can be used by your advisors and heirs to set up or continue your giving and fulfill your values beyond your lifetime.

3. Consider how a DAF account might be used

Once you’ve set up your will or trust and defined your charitable goals, you may want to use a donor-advised fund account during your lifetime to integrate charitable planning into your estate plan.

What is a DAF? It’s both a public charity and a vehicle for granting to other charities. A DAF account can be used by one person or multiple individuals, including family members. Contributions to an account may also be invested for potential growth that’s tax-free, helping you have more to grant to charities over time.

After opening a DAF account, you can make irrevocable contributions during your lifetime and claim a tax deduction for them. The DAF account can also be named as beneficiary in your will, trust, or pay-on-death instruments and receive contributions this way. You can also name individual successors and recommend charitable beneficiaries on your account to receive grants after your passing. All of this enables your charitable intent to carry forward seamlessly, providing confidence and peace of mind.

Why a DAF? A DAF is a public charity, which means it can:

Support multiple charitable organizations through a donor’s grant recommendations

Continue beyond your lifetime through named successors on the account or recommended charitable beneficiaries

Adapt to your family’s evolving values

It combines life and legacy planning into a single charitable giving tool, with the added advantage of investing contributed assets to potentially grow charitable gifts over time.

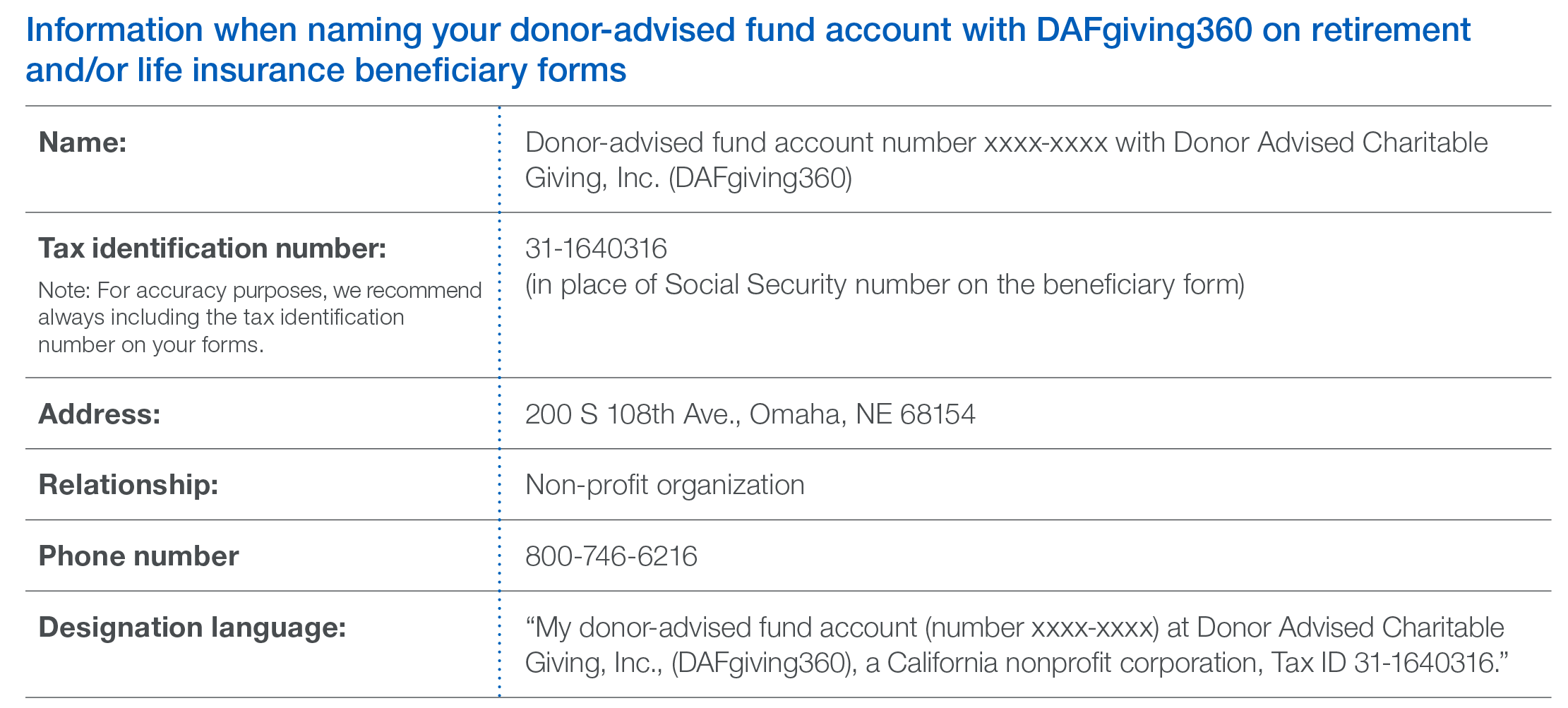

Note: If you plan to name a DAF—or any charity—as a charitable beneficiary, be sure to inform them. They’ll need to confirm they can accept the future gift and understand your giving wishes, so your charitable legacy is honored as intended. Make sure your succession plan is updated in both your will/trust AND your donor-advised fund account, so that your charitable donations can be distributed based on your preferences.

Include this information when naming your donor-advised fund account with DAFgiving360 as a charitable beneficiary:

4. Select which assets will be given to charity

Not all assets are created equal when it comes to charitable gifting through your estate plan. Donating certain types of assets over others can offer tax advantages you may wish to consider.

For example, some assets, such as retirement accounts and commercial annuities, are known as income in respect of a decedent (IRD) assets. This means a person earned the money or had a right to it before they died, but it wasn’t paid out until after.

These assets are still taxed, which means your heirs would have to pay income tax on them. However, if you contribute IRD assets to a DAF account or charity, they can transfer tax-free. This allows you to make a bigger charitable impact while potentially reducing the tax burden on your loved ones.

Other assets, like stocks or real estate that have gained value, currently receive a “stepped-up basis” at death. These assets may be more valuable to your heirs since the base value, for future calculation of capital gains tax, is being reset to the higher appreciated value at death.

The point is this: it’s important to be strategic when deciding which assets to contribute to a DAF and which go to other beneficiaries. Choosing the right assets to fund a DAF account can maximize charitable impact and minimize tax liability. For a subset of donors, your estate may heavily rely on a claimed charitable deduction to reduce or offset tax liability, so charitable gifting is essential, no matter the asset.

If you’re considering donating more complex assets (such as real estate or a private business interest) or collectibles (like that 1966 burnt orange Ford Mustang with pony interior), it’s best to speak with a representative from the DAF or other charity to obtain donation guidance. Some additional steps may be required to complete the transfer.

5. Have a succession plan on your DAF account

Okay, you’ve done all the hard work! You’ve built a thoughtful estate plan, clarified your charitable goals, established a DAF account, and identified assets to be given to charity. Now it’s time to take the final step: create a succession plan for the DAF account. A DAF can extend your charitable values well beyond your lifetime, but only if you’ve created a plan for what comes next.

You may want to name one or more successors on your DAF account, like family members or trusted advisors, who can continue recommending grants to charities that reflect your legacy and intentions.

As you consider your legacy and values, bring your chosen successors into the conversation early. Share the “why” behind your giving so they are equipped to carry it forward and the thoughts and values you identified in step 2.

If you already know the charities you wish to receive grants in the future, you may also recommend them as one-time or ongoing charitable beneficiaries.

It’s also important to connect with the DAF sponsor on all succession options. They can help ensure that your intentions are feasible, honored, and comply with IRS rules so that the charitable assets are set up to support giving for years to come.

Next steps for charitable estate planning

To continue diving into the topic of charitable estate planning, here are some additional resources:

Download the full DAFgiving360 Giving Guide

Learn more about Charitable Remainder Trusts

Learn more about Charitable Lead Trusts

Explore non-cash asset donations

For questions or assistance with philanthropic planning or charitable giving, you and your advisors may:

Call the DAFgiving360 Donor Services team at 800-746-6216

Follow DAFgiving360 on LinkedIn

Coauthors:

Caleb Lund, CAP®

Director of Charitable Strategies Group

DAFgiving360TM

Austin Jarvis, JD, MBA, CTFA

Director of Tax, Trusts, and Estates

Schwab Center for Financial Research